The VIX Is Screaming to GET IN NOW! And Don’t Miss Our FREE Saturday Event!

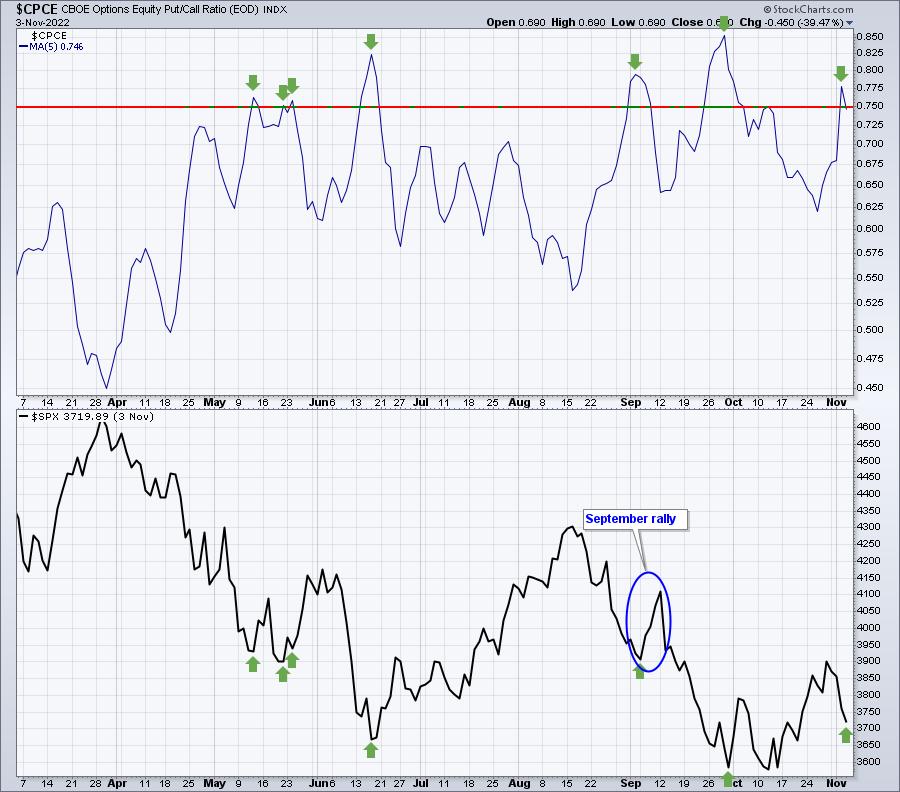

My two favorite sentiment indicators are (1) the 5-day moving average of the equity-only put-call ratio ($CPCE) and (2) the Volatility Index. On September 6th, I wrote about the elevated CPCE likely providing a short-term market bottom and it did. The S&P 500 jumped 5% in a week. That same CPCE chart is elevated once again, potentially signaling another short-term market rally. I don't use the CPCE 5-day moving average as a long-term bottom signal as sentiment can reverse quickly. But check out the timing here:

This isn't my opinion, it's reality. When we swing too far to the downside and options traders become too pessimistic, we bounce. That's been the history of the stock market.

Well, now the Volatility Index ($VIX) is joining the party. The VIX represents the "expected" volatility over the next month. From the Chicago Board Options Exchange (CBOE), here's how they describe the calculation of the VIX:

"CBOE calculates the VIX Index using standard SPX options and weekly SPX options that are listed for trading on CBOE options. Standard SPX options expire on the 3rd Friday of each month and weekly SPX options expire on all other Fridays. Only SPX options with Friday expirations are used to calculate the VIX Index. Only SPX options with more than 23 days and less than 37 days to the Friday SPX expiration are used to calculate the VIX Index. These SPX options are then weighted to yield a constant maturity 30-day measure of the expected volatility of the S&P 500 Index."

In other words, the CBOE looks ahead at the pricing of SPX options with roughly 30-day maturities to determine the "expected" volatility. As the S&P 500 sells off, expected volatility increases as premiums rise on the options that meet that 23 to 37 day criteria.

This is why there is usually an inverse relationship between the S&P 500 and the VIX. As prices drop, moves in the S&P 500 escalate, causing future options to become more expensive, thus increasing the VIX. The opposite typically holds true as well. Historically, the S&P 500 rises in a much more boring fashion, so as it moves up, the price of options is less expensive, resulting in a declining VIX. Again, it's that inverse correlation that we expect.

Occasionally, however, we see the S&P 500 and VIX move together, but it doesn't last long. It does provide interesting signals, though:

We've seen essentially three signals prior to the one that triggered yesterday. The March reversing signal worked beautifully. The August and October signals worked, but the first signal each of those two months saw a bit more upside before a 2nd signal corroborated the 1st. Selling kicked in after that 2nd signal. Now the S&P 500 is turning lower, BUT SO IS THE VIX. That's resulted in another positive correlation reading. We should expect to see the S&P 500 turn back higher.

Will we see another big rally ahead? There's certainly no guarantee, but both of my favorite sentiment indicators are pointing to that.

There's ONE LAST CHANCE for you to join me at tomorrow's FREE virtual live event, "Understanding Market Manipulation". The event begins at 10am ET, but you MUST register with your name and email address. CLICK HERE for more information and to register. And I'll see you tomorrow morning!

Happy trading!

Tom