At the Edge of Chaos: Central Banks, 1 – Santa, 0. Bond Traders Laugh

This is my final Market Summary for 2022. I will be back in January; subscribers can expect portfolio summaries and intermittent alerts as usual.

Here are some final thoughts for the year:

In the short term, mostly because of technical reasons – the market is very oversold – we may see some sort of bounce. If there is a bounce, it may be over in a matter of hours, a matter of days, or somewhere in between. On the other hand, there is the possibility that the recent selling may lead to something that lasts longer on the upside if enough short sellers can be pushed into covering. But, as we've seen for the entire year, if real buyers don't follow short-covering rallies, the downtrend will prevail.

Longer-term, unless something very unusual happens, a new bull market won't arrive until the Fed takes its big boot off of the market's throat.

Central Banks: 1 – Santa: 0. Bond Traders Laugh.

It looks as if the Fed and global central bankers don't like the idea of a Santa Claus rally, as, even though there are signs of a slowing economy and, perhaps, a slowing of the rise in the rate inflation, interest rates are going even higher.

Last week in this space, I wrote: "things can change and will likely (do so) instantly in this market as the Federal Reserve's December 14 interest rate announcement and future guidance about interest rates unfolds. The response will likely shape what the stock market does for the remainder of the seasonally bullish year-end period and into 2023."

And that's exactly what happened after the most recent rate increase and promise of more to come, as stocks collapsed, except in some areas of the market that benefit from lower bond yields. On the other hand, bonds are betting on a recession.

However, it's still possible to make money in stocks during periods of rising interest rates. You can see when and how to fight the Fed and win in my latest Your Daily Five video here.

Bond Traders Laugh as the Fed Fights the Wrong Fight

The bond market doubled down on its recession bet after the Fed's most recent rate increase and its promise to keep hiking, while keeping rates high for a long time. The Fed thinks inflation is still too high, which it is at the grocery store mostly, or if you you're looking for a place to live, while bond traders are openly betting on what now has to be seen as a fairly sizeable recession.

Here is why we are where we are. The Fed is fighting inflation, which has resulted from the "just-in-time" supply chain trend spawned in the late 1970s, which gathered steam in the 1980s, as if it was a traditional inflationary spiral. It's not. This inflation crisis developed under the surface over decades because large corporations moved many of their manufacturing operations to China, India, Vietnam, and other countries where labor costs were cheaper. As long as none of the underlying factors changed, inflation remained fairly tame and profits remained high. But the potential for inflation continued to build up quietly, much like a volcano's slow lava buildup over time prior to an eruption.

Of course, COVID destroyed the supply chain and laid bare the fact that the manufacturing capacity in the U.S. had been significantly reduced, while the demand for products remained constant and is likely to increase as the population changes and relocates, and the economy evolves from its current technology-dependent dynamic to one in which trades, construction, and manufacturing become larger contributors to GDP.

The take-home message is that today's inflation is more due to the supply side than the demand side. If you don't make enough stuff for people to buy, even steady demand will drive prices up. But when your supply chain collapses due to a pandemic, all bets are off. Meanwhile, if you print trillions and give people stimulus checks, you're just adding napalm to an already-hot fire as, at that point, more money is indeed chasing fewer goods.

So the stimulus isn't really the cause of the inflation. It was the spark that led to the eruption.

All of which brings me back to why bond yields are falling. The fact is that bond traders know that, since the stimulus checks are no longer a factor, this inflation is again due to a long-standing supply chain-related supply side imbalance. Moreover, even though some manufacturing is coming back to the U.S., much still remains abroad – where costs are also rising as the emerging market workers begin to ask for more money and better working conditions.

So, here's where it all comes together.

The Fed is going to raise interest rates until the Fed Funds rate is somewhere above 5%. In addition, the central bank also noted that it's not going to lower rates for a good while even after it stops raising them, maybe into 2024.

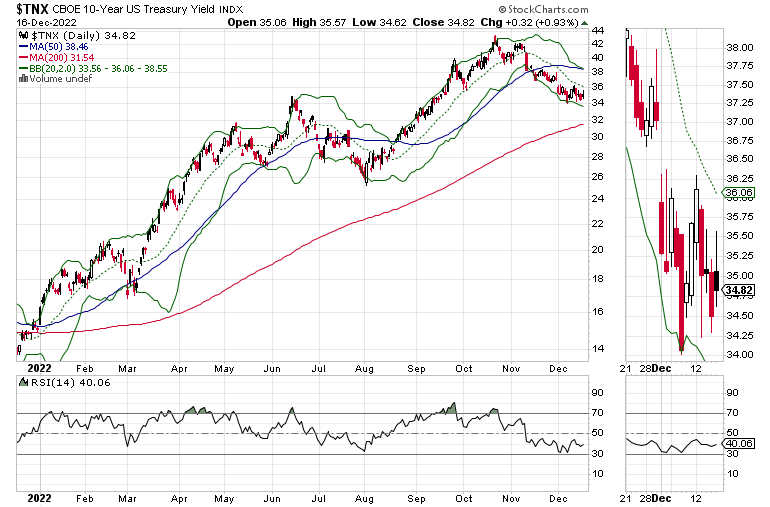

The bond market sees the central bank's stated goals as an opportunity to bet on a big economic contraction, as yields fell below 3.5% on the U.S. Ten Year note (TNX).

The message from the bond market is pretty clear:

You can raise interest rates until you are blue in the face, but, if no one builds factories to make the things people use domestically, you're just raising interest rates and killing the stock market; and The lower stock prices go, the more you will hinder the wealth effect based on the MELA system (Markets, Economy, Life Decisions, and Algos) – as the value of 401 (k) plans will continue to fall and people will reduce their expenses.So, the more the Fed tightens, the lower bond yields will likely fall. And it's all because the Fed doesn't have the power to change the way corporations seek to increase their profit margins, or to control politicians who like to spend money they don't have. Thus, all the Fed can do is raise rates, kill stocks, and hope someone changes the way they do what they do.

At the moment, corporations are starting to see the light. But, the restructuring of the U.S. economy is not likely to happen fast.

Finally, according to a recent report by the Philadelphia Fed, the monthly employment reports have overstated job growth by one-plus million jobs as of Q2, 2022. All of which suggests that just as the Fed is ramping up more rate hikes, the bad economic news is about to ramp up.

And that's why bond traders are laughing.

Welcome to the Edge of Chaos:

"The edge of chaos is a transition space between order and disorder that is hypothesized to exist within a wide variety of systems. This transition zone is a region of bounded instability that engenders a constant dynamic interplay between order and disorder." – Complexity Labs

NYAD Again Fails at 200-Day Moving Average

Last week in this space, I noted: "the NYAD, as it did during the summer rally, has failed to move above its 200-day moving average, a negative development. It also broke below its 20-day moving average and is about to test its 50-day line. A failure at the 50-day line will likely trigger bigger selling in stocks."

Indeed, NYAD ended last week right at its 50-day line, leaving everyone in suspense. But the usual panic signs, a collapse in liquidity and a huge rise in VIX, did not develop. Liquidity is surprisingly stable, as the Eurodollar Index (XED) has been trending sideways to slightly higher for the past few weeks.

The CBOE Volatility Index (VIX) yawned through the market's meltdown. When VIX rises stocks tend to fall as put volume rises, that is a sign that market makers are selling stock index futures in order to hedge their put sales to the public. A fall in VIX is bullish, as it means less put option buying.

The S&P 500 (SPX) saw aggressive short-selling (falling ADI) and a new low developed in On Balance Volume (OBV) suggesting that sellers and short sellers were very active.

The Nasdaq 100 index (NDX) also tumbled, but remained rangebound between the 11,000-12,000 trading range, but did break below its 50-day moving average.

To get the latest up-to-date information on options trading, check out Options Trading for Dummies, now in its 4th Edition—Get Your Copy Now! Now also available in Audible audiobook format!

#1 New Release on Options Trading!

Good news! I've made my NYAD-Complexity - Chaos chart (featured on my YD5 videos) and a few other favorites public. You can find them here.

Joe Duarte

In The Money Options

Joe Duarte is a former money manager, an active trader, and a widely recognized independent stock market analyst since 1987. He is author of eight investment books, including the best-selling Trading Options for Dummies, rated a TOP Options Book for 2018 by Benzinga.com and now in its third edition, plus The Everything Investing in Your 20s and 30s Book and six other trading books.

The Everything Investing in Your 20s and 30s Book is available at Amazon and Barnes and Noble. It has also been recommended as a Washington Post Color of Money Book of the Month.

To receive Joe's exclusive stock, option and ETF recommendations, in your mailbox every week visit https://joeduarteinthemoneyoptions.com/secure/order_email.asp.