At the Edge of Chaos: Contrarians Investors with a Regional Bias Will Outperform Traditional Macro Strategies in 2023

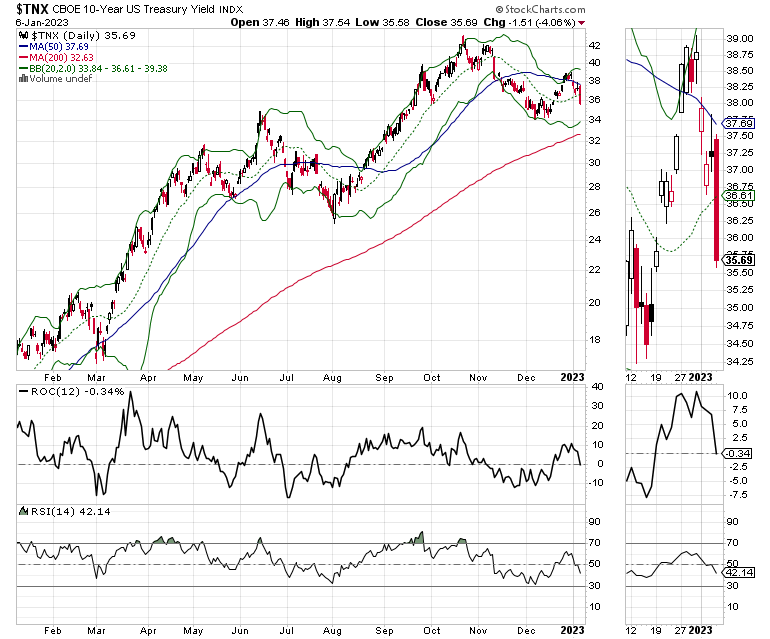

Just as many investors were getting ready to throw in the towel, the Federal Reserve may be signaling that it's getting close to stopping its rate hikes. Meanwhile, the latest jobs report suggested that wage gains are slowing. The combination of rising pessimism and a potential change in behavior from the Fed ignited a nice Friday rally in stocks, as well as a nifty reversal in the U.S. Ten Year Note yield (TNX).

However, if inflation shows signs of picking up steam once again as the latest batch of CPI numbers are released, we can expect more hawkish talk from the Fed, a potential reversal in TNX, and a new down leg in stocks.

Data Points to Slowing Economy

Bond yields are well off of their recent highs. That's because there is a growing body of private macro data, especially recent PMI and ISM numbers, that suggest that the U.S. economy has been slowing for months and, perhaps, that slowing is accelerating.

There is also a regional variation in the economy which I detail below, and which the central bank and most private analysts aren't commenting on. It's that regional variation that could muddle the waters for the Fed while providing a potential area of profits for investors who know what to look for.

From a trading standpoint, the external macro background, such as the Fed's actions and economic data, are important. But what happens in the stock market is most important. Therefore, as a contrarian investor, I will suggest the following two caveats for the year:

Look to invest in down-and-out sectors where those who are panicking are bailing out; and Consider a regional orientation to where you put your money.First, let's look at some key economic data from a contrarian point of view.

ADP Data

While the PMI and ISM data does not break the data down by region, the most recent ADP Private Employment Report does. Certainly, the headline which notes that the private sector created 235,000 was a market mover, as investors saw this as bad news which would make the Federal Reserve continue on its "higher for longer" trek for interest rates. Still, the number was close to the government's data released a few days later.

A closer look at the data (see page 2 of the ADP report) illustrates my point, as the private job growth was in the Northeast (54,000 jobs added), the Midwest (70,000 jobs), and the South (253,000 jobs). Meanwhile, the West lost 142,000 jobs.

U-Haul Data

Comparing the ADP data to U-Haul's 2022 One-Way destination data shows a remarkable correlation, as Texas, Florida, and the Carolinas were the leading regions. Moreover, California, Illinois, and New York led the way for one-way departures.

A further parsing of the ADP data shows that the New England area (roughly including New York) only had 2,000 jobs added, while the West North Central area (including Illinois) added 9,000 jobs.

Even more interesting was the fact that the highest jobs numbers in the ADP under goods-producing sectors was 41,000 construction jobs. ADP did not list where the construction jobs were added, but I would not be surprised if most of them were in the south.

Split Decision

The Fed looks at data for the whole U.S. and does factor in global data as well. The problem with that approach is that there is a wide-ranging regional difference in the economic activity in the U.S. This data is no longer anecdotal. Recent private sector reports, as well as U.S. Census data, confirm what the U-Haul and ADP data are saying, which is that people are leaving certain regions of the U.S. and moving permanently to others.

In other words, the current data which the Fed relies on, GDP, and other national statistics may not show an actual recession, because the economic activity in the sunbelt may be growing at a decent clip while the New York, Illinois, and the West Coast may actually be struggling. This creates a potentially messy situation for the Fed as it ponders what to do about the future of rate increases. When the recession hits, it will likely hit the areas where people are leaving harder than the areas where people are migrating.

Thinking Regionally

Since the Fed is thinking one-size fits all, and the reality on the ground may be significantly different based on regional realities, investors who think regionally are more likely to fare well in 2023 than those who follow the national macro, which is widely followed on Wall Street and at the Fed. What that means is that those sectors who benefit from the migration and the subsequent outcomes are the most likely to deliver the best results, as long as the Fed remains in its "higher and longer" mode.

Here's an example of what I mean. If people are moving to new areas of the country, there will be a need for infrastructure, as roads will need repairs and expansion, utilities will need to grow their grid, and the demand for energy in those areas will increase. Most of all, jobs will need to be created in order to support the surge in population.

An overlooked area of the stock market for decades has been that of building materials. Yes, cement, concrete, lumber, insulation, glass, and the machinery to deploy them will be central to the way forward for areas of the U.S. which will face the accommodation of growing populations. And a one-stop shop to consider might be the Materials Select Sector SPDR ETF (XLB).

As you can see by the price chart, XLB has been a fountain of relative strength of late. In fact, it's delivered a nice rally since its most recent bottom in October 2022. Accumulation/Distribution (ADI) has been very steady, which means short-sellers are finding other places to ply their wares. Meanwhile, On Balance Volume (OBV) has bottomed out, which means that sellers are just about finished as well. This creates a potentially bullish scenario for this sector ETF, especially if it can clear the 200-day moving average and the large Volume by Price bar (VBP) around $82.

The bottom line is that in this market, even as the Fed continues to raise interest rates, there are areas of opportunity. Investors just have to dig deeper and consider the macro effects of what's happening on the ground.

Welcome to the Edge of Chaos:

"The edge of chaos is a transition space between order and disorder that is hypothesized to exist within a wide variety of systems. This transition zone is a region of bounded instability that engenders a constant dynamic interplay between order and disorder." – Complexity Labs

NYAD Challenges 200-Day Moving Average

The New York Stock Exchange Advance Decline line (NYAD) broke above its 50-day moving average on 1/6/23 and is on the verge of challenging its 200-day moving average. A sustained move above the 200-day average would be a very bullish development. Note that all counter-trend rallies in this bear market have failed at the 200-day moving average.

For its part, the CBOE Volatility Index (VIX) continues to roll over. This is also bullish. When VIX rises, stocks tend to fall, as rising put volume is a sign that market makers are selling stock index futures in order to hedge their put sales to the public. A fall in VIX is bullish, as it means less put option buying.

Liquidity remained surprisingly stable, as the Eurodollar Index (XED) has been trending sideways to slightly higher for the past few weeks.

But the current situation is slightly different. You can see that shares of D.R. Horton and Lennar fell for several months in 2022 as the U.S. Ten-Year-Old Note yield rose. However, the stocks responded well when the yields reversed. You can see that RDFN shares have yet to recover.

The S&P 500 (SPX) found support at 3800, and is now testing its 20-, 50-, and 200-day moving averages. Accumulation/Distribution (ADI) has stabilized, but On Balance Volume (OBV) remains near its recent lows. ADI suggests short sellers are making quick profits and getting out, while OBV suggests that sellers are not quite done yet.

The Nasdaq 100 index (NDX) continues to lag SPX badly. It is still possible that it may have made a triple bottom, with the 10,500-10,700 price area bringing in some short covering. The problem is that the 12,000 area and the 200-day moving average, together, form a sizeable resistance band.

To get the latest up-to-date information on options trading, check out Options Trading for Dummies, now in its 4th Edition—Get Your Copy Now! Now also available in Audible audiobook format!

#1 New Release on Options Trading!

Good news! I've made my NYAD-Complexity - Chaos chart (featured on my YD5 videos) and a few other favorites public. You can find them here.

Joe Duarte

In The Money Options

Joe Duarte is a former money manager, an active trader, and a widely recognized independent stock market analyst since 1987. He is author of eight investment books, including the best-selling Trading Options for Dummies, rated a TOP Options Book for 2018 by Benzinga.com and now in its third edition, plus The Everything Investing in Your 20s and 30s Book and six other trading books.

The Everything Investing in Your 20s and 30s Book is available at Amazon and Barnes and Noble. It has also been recommended as a Washington Post Color of Money Book of the Month.

To receive Joe's exclusive stock, option and ETF recommendations, in your mailbox every week visit https://joeduarteinthemoneyoptions.com/secure/order_email.asp.